One day, 4 years ago, my partner was stressed out, in a bad mood and not doing very well. On a romantic whim, which sometimes only comes with new love, I decided to take him out somewhere nice. My partner and I enjoy going out for a nice meal and drinks, so I decided to pick somewhere very Los Angelean and romantic.

The Bonaventure.

There are glass windows, beautiful views of the smog-filled LA skyline, white table clothes and suited up waiters. I knew it was fancy, but how expensive could it be? I was on a mission, Operation Make Boyfriend Feel Better.

We arrived at the restaurant, impressed with the views and excited to try something new. I looked around and we were definitely the youngest people there. Business types, socialites and other cosmopolitan people filled the room. We sat down, placed our white napkins in our laps and looked over the menu.

Oh, wait, $20 for a burger?

$14 for a martini?

The math was already too much and my boyfriend quickly saw the discomfort on my face. I looked around in a panic and saw all the groups of people having fun, spending money frivolously. Clearly, we did not fit in. What was I thinking? Just then, a man sitting across from us, eating dinner by himself, gave us a quick smile of acknowledgement.

My boyfriend and I agreed to share a burger and get only one drink each to keep our “costs low”. This was already not the romantic evening I had imagined, but we were going to make it work. After all, it was pretty comical.

My boyfriend was impressed by my efforts and we made the most of it. We both enjoyed the strongest martini of our lives (for that price, it better be) and we shared the tiny, gourmet burger which was far too small for our growing appetites. After thoroughly enjoying ourselves, I saw the waiter come over with the bill. I was nervous, but already did the math in my head and justified the expense. The waiter came over, not to deliver the bill, but to let us know the gentleman sitting alone had decided to pay for our entire meal and left a note. I looked over to where he was sitting, and he was gone. In a matter of seconds, my boyfriend and I start weeping in front of the waiter. He left the note and walked away.

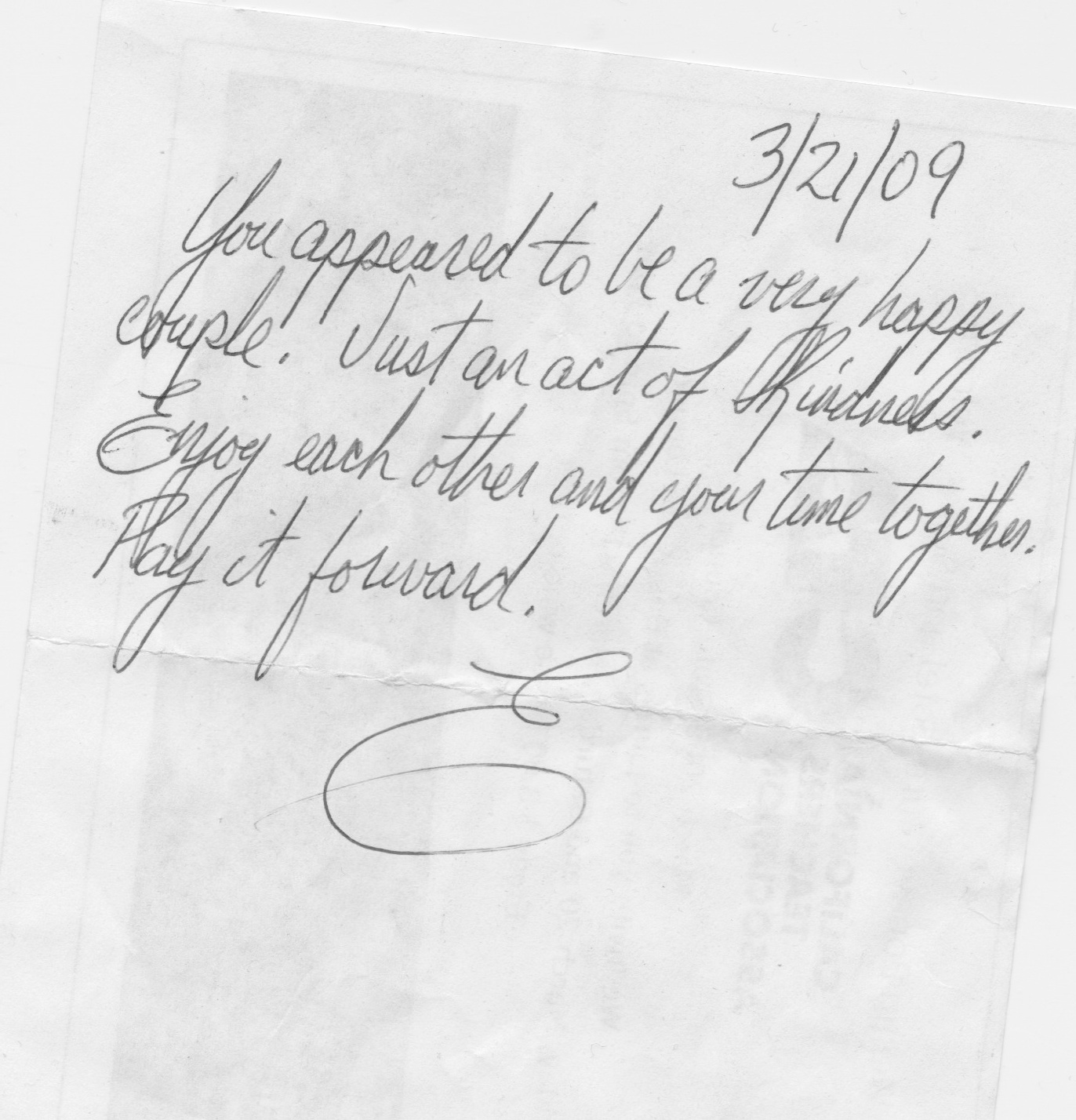

The note read: You appeared to be a very happy couple. Just an act of kindness. Enjoy each other and your time together. Pay it forward.

The tears really started coming now. After a day full of depression and misanthropy, we experienced such a generous random act of kindness. We never spoke to the man in question; I don’t know who he is or why he was compelled to do that for us. The note was written on the back of a California Teacher’s Association flyer. All of a sudden I had an intense urge to know this man—to know who he was and why he did what he did. I realized I had no way of getting in touch with him and that is how he wanted it. My boyfriend and I cried for a long time, simply amazed by the power and beauty of strangers. That night single-handedly changed our ways of thinking and inspired us to pay it forward and commit other random acts of kindness.

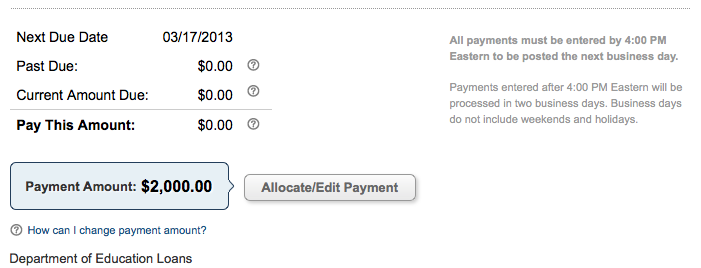

In my last post, I talked about wanting to pay off debt so that I could be more generous. Although money can buy a lot of things, there are plenty of ways to pay it forward and commit random acts of kindness that don’t cost money or are low cost. For example, two years ago, I organized a donation drive for homeless women. You’d be amazed at the simple things they wanted—combs, toothbrushes, lotion. You can find those things at the 99 cent store! I organized all my friends to contribute in honor of all the fabulous women in their lives. It meant a lot to those women having new things; items I wouldn’t think twice about. Recently, after accruing some serious mileage doing long-distance, I decided to fly my mom up here with my miles. It cost me $2.50 with tax. A few weeks ago, I saw a women on the street crying. I asked her if she was alright and she said “no”. She told me that she was stranded and trying to get home and didn’t have any money. She was asking for just a little bit of money from people and she told me people were so rude to her. They said things like, “Get a job”, “You’ll just use it for drugs” and other cruel things. Sadly, I didn’t have any money to help her either. I deliberately carry no cash or cards as a mechanism to not spend money. I felt so bad, but she said she was so touched that I even stayed with her a while to chat and asked how she was doing. I gave her some resources and let her talk it out. This was a woman crying her eyes out in the street, and no one wanted to help.

Sometimes paying it forward is as simple as a smile. Or asking someone how they are doing.

To me being debt free means being in a position to help others—because I know so many people have helped me when I needed it. We are not singular beings existing on individual planes….sometimes reaching out can mean the world to someone. I look forward to more random acts of kindness, paying it forward and paying off debt! To help those causes and people I am truly passionate about.